Condo vs. Co-op in NYC (2026 Guide): Which One Is Right for You?

If you’ve been scrolling through New York City real estate listings, you’ve hit the wall. It’s the "C-word" divide. You find a gorgeous pre-war gem with a price tag that seems too good to be true—Co-op. Then you see a sleek glass tower with a balcony, but the price makes your eyes water—Condo.

In a market as fast-paced as 2026, where NYC housing prices have jumped 10.3% year-over-year, choosing between these two isn't just a lifestyle choice; it’s a high-stakes financial decision.

Let’s pull back the curtain on the "Great NYC Divide" and see which one actually fits your 2026 goals.

Condo vs Co-op: The Key Ownership Difference

The biggest shock for first-time buyers is often what they actually own at the end of the day.

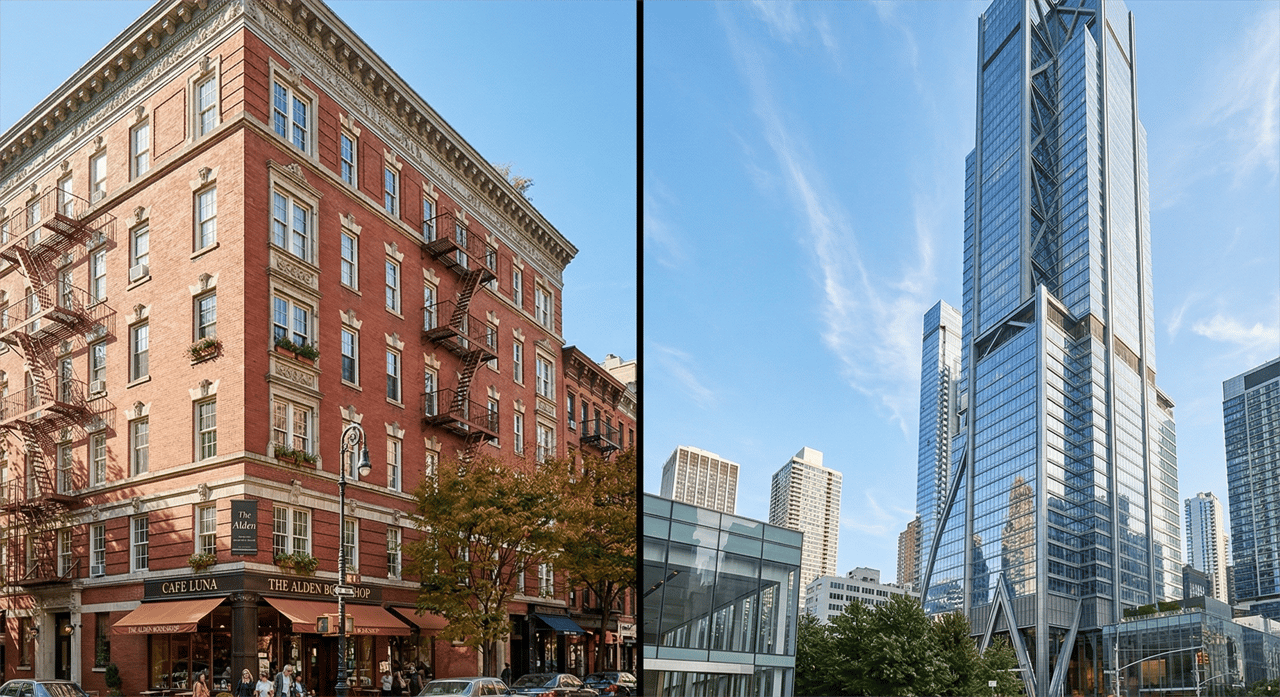

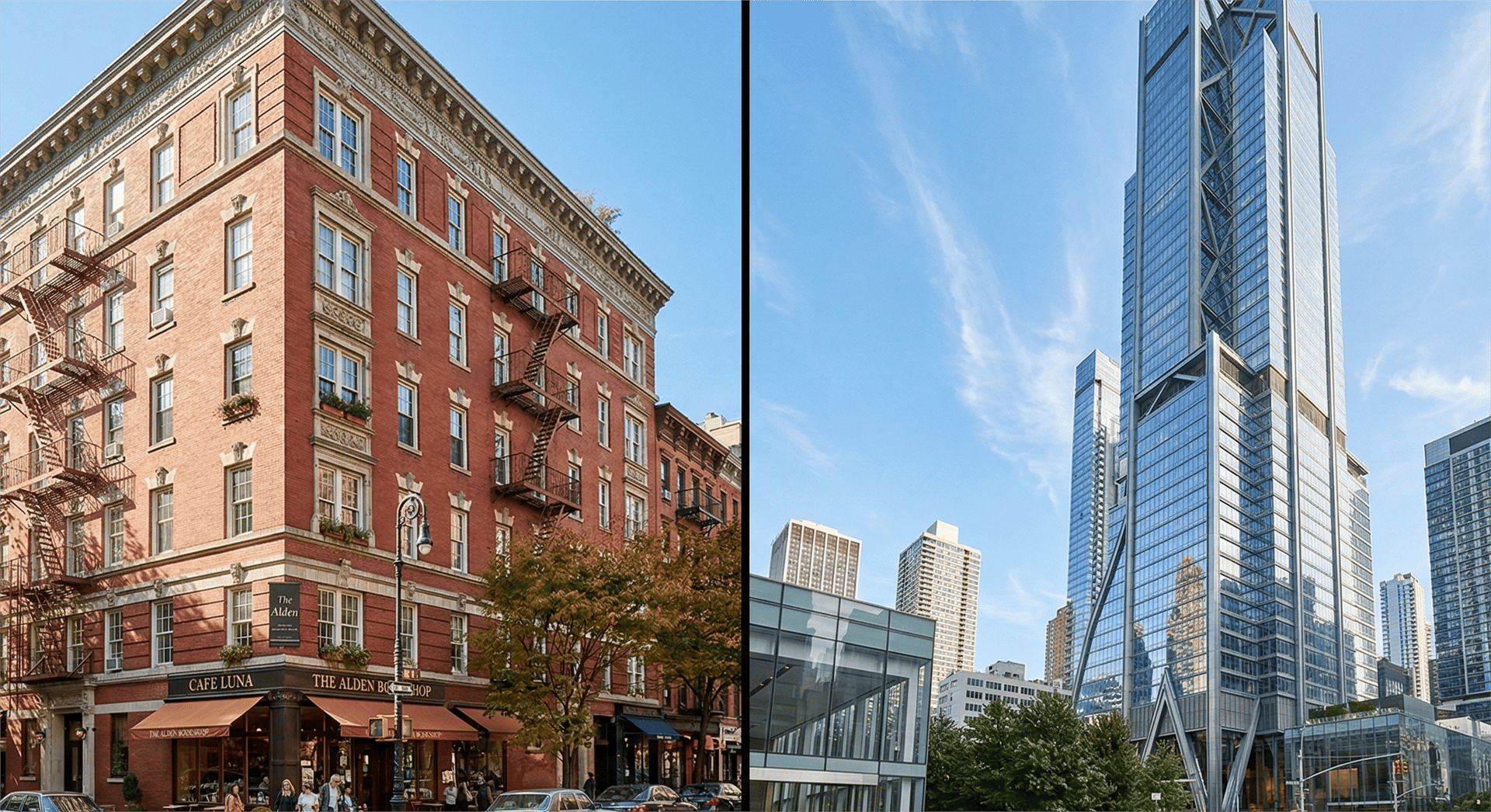

- The Condo (The "House in the Sky"): Buying a condo is traditional homeownership. You receive a deed to your specific unit and own a percentage of the common areas. It is real property.

- The Co-op (The "Exclusive Club"): You don’t technically own your four walls. Instead, you buy shares in a corporation that owns the building. Those shares grant you a "proprietary lease," giving you the right to live in your unit as a "shareholder-tenant."

NYC Condo vs Co-op Prices in 2026

In today’s market, the price gap is substantial. As of early 2025, the median condo price in NYC hit $1,068,220, while co-ops sat much lower at $505,917.

What’s trending now?

While co-ops make up roughly 70% of Manhattan's owned housing stock, condos are seeing massive upward pressure. In Q1 2025 alone, condo prices increased 11.3% quarter-over-quarter compared to 9.5% for co-ops. Modern buyers are increasingly flocking to condos for their luxury amenities and the "brand-new" allure of glass towers.

Condo vs Co-op Comparison Table (NYC Buyers Guide)

|

Feature |

Co-op |

Condo |

|

Purchase Price |

Often 25–30% lower per sq. ft. |

Generally higher |

|

Down Payment |

Usually 20% to 50% |

As low as 10% |

|

Closing Costs |

Significantly lower |

Higher (due to Mortgage Recording Tax) |

|

Monthly Fees |

"Maintenance" (Includes property taxes) |

"Common Charges" (Taxes paid separately) |

Pro Tip: While co-ops have a lower barrier to entry on price, they demand more "liquid skin" in the game. Most boards require you to have 1–2 years of mortgage and maintenance payments in cash reserves after you’ve already paid the down payment.

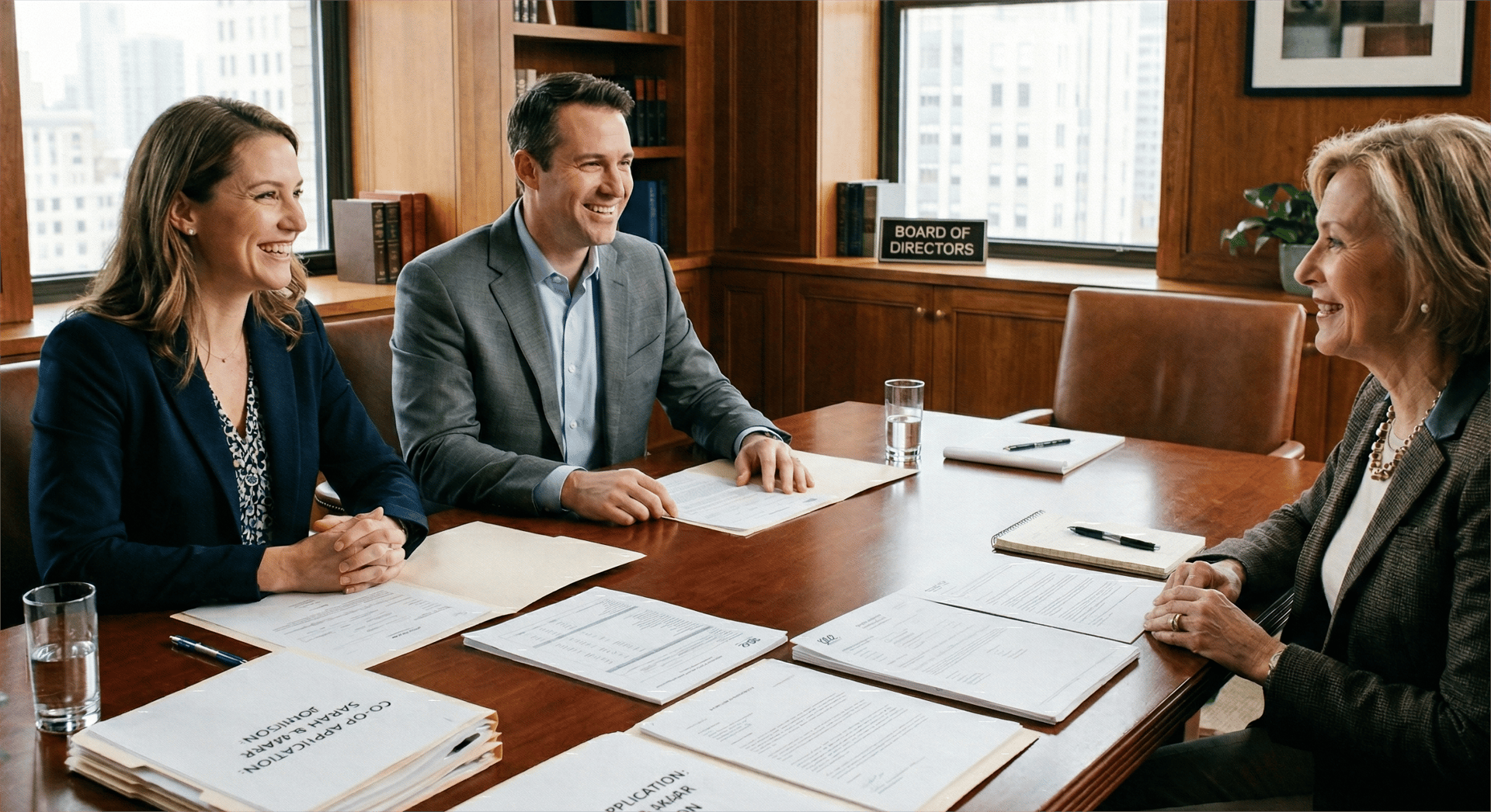

NYC Co-op Board vs Condo Board: Approval Differences

In NYC, having the money isn't always enough. Sometimes, you have to be "vetted."

Condo Boards

- Approval Process: Condos require an application and financial documents, but the process is far less restrictive.

- The Interview: There is typically no interview for a resale condo.

- Power: The board has a "Right of First Refusal". To stop you from buying, they must buy the unit themselves at your offered price, which is extremely rare.

Co-op Boards

- Approval Process: You must submit a "board package" with years of tax returns, bank statements, and personal and professional reference letters.

- The Interview: This is a mandatory meeting where board members meet you to ask about your background and reasons for choosing the building. It can feel invasive, as they examine your finances and lifestyle.

- Power: Co-op boards have broad discretion. They can reject you for almost any non-discriminatory reason—often without explaining why—even if you are paying all cash.

Investment & Flexibility: Are You a "Settler" or a "Nomad"?

The 2026 market is all about agility. If there's a chance you'll relocate in a few years, your choice matters.

Choose a CONDO if:

-

You are an international buyer: Condos are much friendlier to foreign funds and allow you to buy through an LLC for privacy.

-

You want a rental asset: Most condos allow subletting from day one, making them ideal for generating income.

You want the "New NYC": Most sleek, glass towers with luxury amenities like roof decks and pools are condos

Choose a CO-OP if:

- You want more "Bang for your Buck": You can often get a much larger layout for the same price as a smaller condo.

- You value stability: Co-ops are less transient because subletting is strictly limited (often only 1–2 years out of every 5).

- You love "Old New York": If high ceilings and pre-war architectural details are your love language, the co-ops of the Upper East and West Sides are calling.

The Bottom Line

If you want the freedom to treat your home like an agile asset—renting it out or selling it with ease—the Condo is your winner. But if you’re looking to plant deep roots in a classic neighborhood and get more square footage for your dollar, the Co-op is a remarkably secure and stable investment.

Which side of the fence are you on?